Kreston SGCO & Team expertise in M&A taxation, corporate regulations, and SEBI compliance, combined with their professionalism and proactive approach, certainly contributed to the seamless process.

We are extremely pleased with the services provided by Kreston SGCO and team for the proposed amalgamation of Vitanosh Ingredients Pvt. Ltd. with and into Lactose (India) Ltd.

I would like to wholeheartedly appreciate prompt and sincere working for filing my family's ITR's.

Kudos to the team.

I am writing this to express my deep sense of gratitude to the Company for filing my family's ITR's , despite the ongoing adverse circumstances.

I owe a special "Thank you", a top notch professional & a caring homemaker mother, who could successfully balance both these difficult roles to complete our filing in a record time.

The team worked meticulously and have timely alerted management for lapses in controls and transactions. We found the team very dedicated, focused and competent to execute the assignment. Glad to have such Team to oversee the transactions & guiding management to take informed decisions.

#gst #tax #ca #compliance #gstscrutiny #gstadvisory #gstreturns #gstupdates #advisoryfirm #krestonsgco #krestonindia #kreston

Amendments to Schedule III of Companies Act 2013 (“Act”) effective from 1st April 2021 DIV I - Indian GAAP Financial Statements DIV II - Ind…

EGR refers to Electronic Gold Receipts issued in exchange for physical gold to facilitate the trading of the noble metal. The introduction of EGR allows…

NFT stands for Non-Fungible Token. A non-fungible token (NFT) is a non-interchangeable unit of data stored on a Blockchain. So, what do you mean by non-fungible? NFTs are…

The Department of Finance, vide its Gazette dated 18th January 2022, has made effective the Income-tax (2nd Amendment) Rules, 2022, introduced therein, adding rule 8AD,…

Securities Exchange Board of India (SEBI), vide its notification dated 3rd August 2021, amended various provisions of the SEBI (LODR) Regulations, 2015. Amendments are applicable…

MCA and Government have made many amendments under the Companies Act, 2013, which came into effect from 01st April 2021 and impacted the financial year…

The government has come up with many changes regarding the creation of a compliance-driven procedure via the interaction of GST returns, e-invoicing system, and e-way…

In the endeavour to further reinforce transparency and better compliance with the law, SEBI has issued the Master Circular on November 23, 2021; here it…

IT Security refers to the methods, tools, and personnel used to defend an organization's digital assets. IT security aims to protect these assets, devices, and…

One more time-consuming process under liquidation, now resolved – ease of compliance A clarification on no requirement for seeking No Objection Certificate or No Dues…

ICAI issues Accounting Standards to guarantee the precision and security of financial statements. For an entity to adopt Indian Accounting standards for the first time, the…

Internal Audit is a foundation of sound corporate governance in organisations and can play an essential role to enhance the following functions: Understanding the Business Management and Accountability Determining…

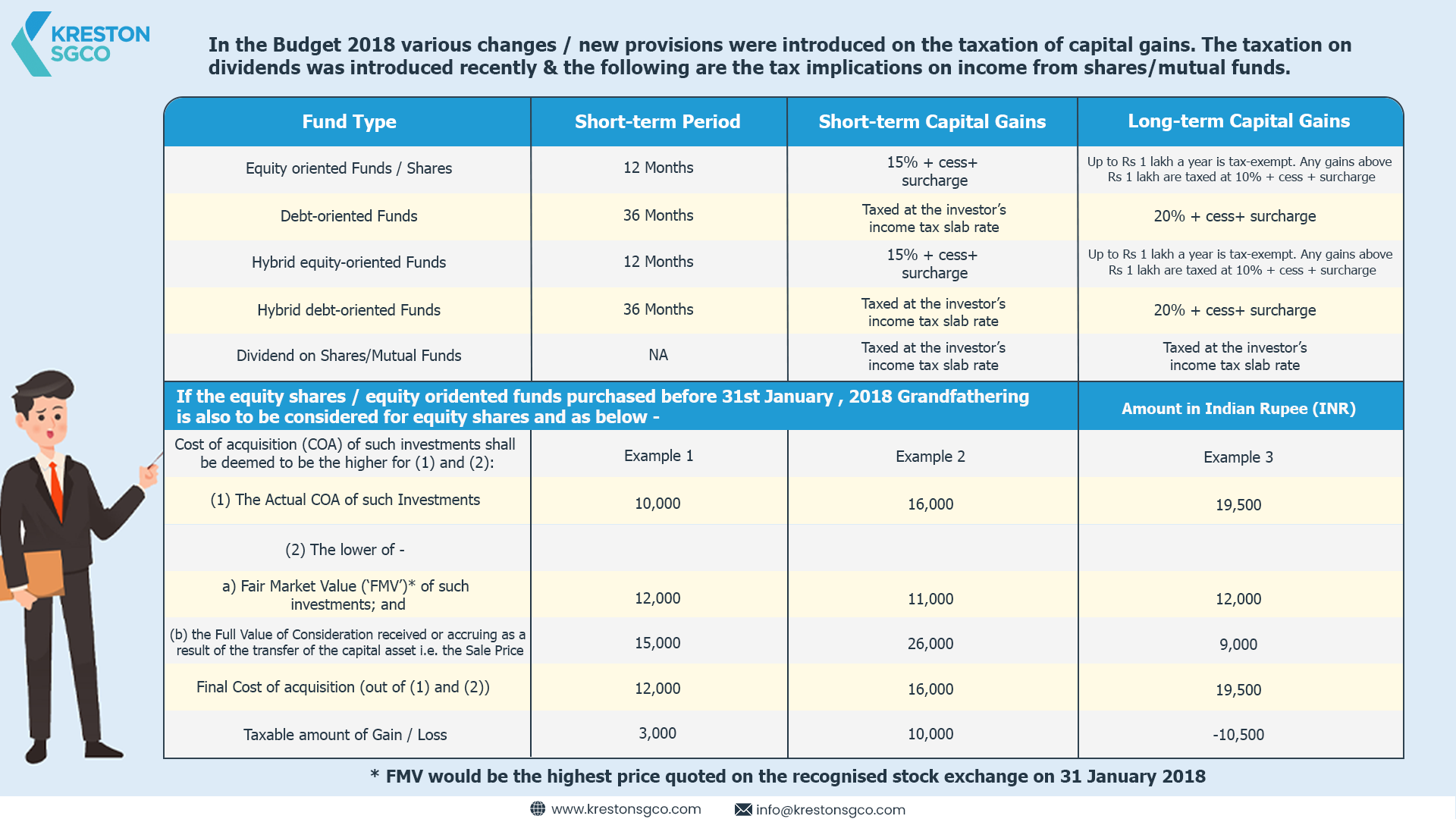

Tax Planning: What Every Investor Needs to Know Our experts have collated comprehensive information for you with the detailed, marked Tax announcement measures levied on…

The Internal Audit (IA) function is crucial for organizations to ensure accurate reporting, manage the risks and controls within an organization's operations, safeguard its Corporate…

Reduced Regulatory Compliance Burden to improve ‘Ease of Doing Business’ Initiative! A welcome move from the Government of India! The exemption from filing return of…

Wellness centres, too, may be liable to GST. Wondering how? Our experts have collated a detailed analysis for you to have a clear understanding of…